The European Central Bank (ECB) has today published the 2018 statistics on non-cash payments.

Payment services1

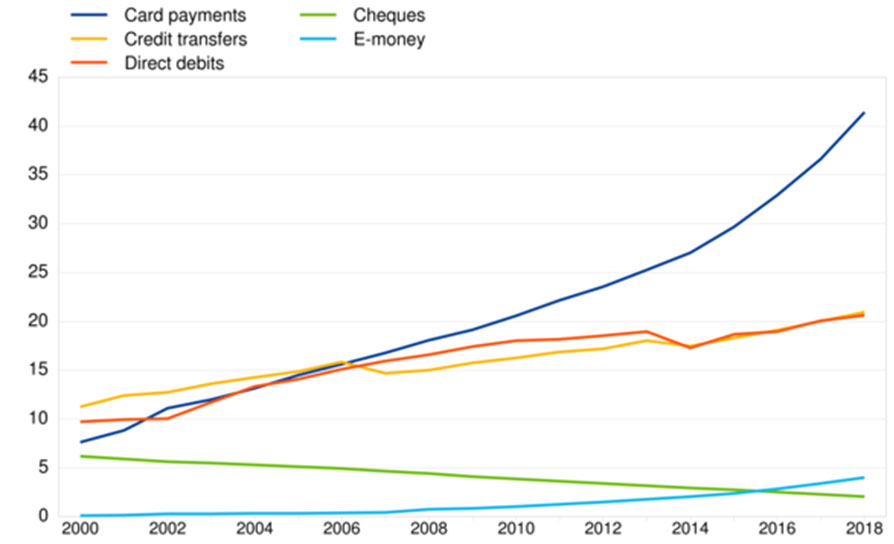

The total number of non-cash payments in the euro area, comprising all types of payment services2, increased by 7.9% to 90.7 billion in 2018 compared with the previous year. Card payments accounted for 46% of all transactions, while credit transfers and direct debits accounted each for 23%.

The number of credit transfers within the euro area increased in 2018 by 4.7% to 21.0 billion. The relative importance of transactions initiated electronically continued to increase, with the ratio of transactions initiated electronically to paper based transactions now standing at around eleven to one.

The number of cards in the euro area with a payment function increased in 2018 by 4.0% to 544.0 million. With a total euro area population of 341 million, this represented around 1.6 payment cards per euro area inhabitant. The number of card transactions rose by 13.0% to 41.4 billion, with a total value of €1.8 trillion. This corresponds to an average value of around €44 per card transaction. Chart 1 below shows the development in the use of the main payment services in the euro area from 2000 to 2018.

The relative importance of the main payment services continued to vary widely across euro area countries in 2018. For example, the highest national percentage for card payments is displayed by Portugal at around 71%, the highest national percentage for credit transfers is found in Slovakia at around 44% and Germany accounts for the highest national percentage for direct debits at around 47% (see Annex).

In 2018, the total number of automated teller machines (ATMs) in the euro area decreased by 0.3% to 0.30 million, while the number of point of sale (POS) terminals increased by 11.2% to 10.5 million.

Retail payment systems

Retail payment systems in the euro area handle mainly payments that are made by individuals, with a relatively low value, high volume, and limited time-criticality.

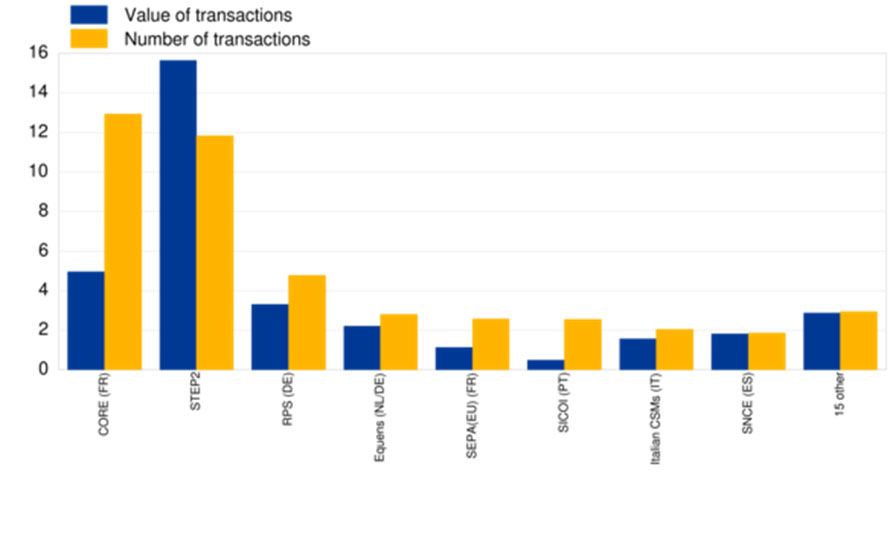

In 2018, data have been reported for 23 retail payment systems within the euro area as a whole. During the year, around 44 billion transactions were processed with a combined value of €34.0 trillion3.

There continues to be a notable degree of concentration in euro area retail payment systems in 2018. The three largest systems in terms of number of transactions (CORE in France, STEP24 and RPS in Germany) processed 67% of the volume and 70% of the value of all transactions processed by euro area retail payment systems. Chart 2 shows the number and value of transactions processed by euro area retail payment systems in 2018.

Large-value payment systems

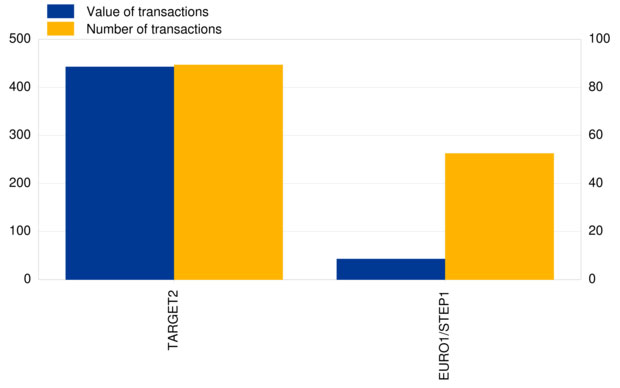

Large-value payment systems (LVPSs) are designed primarily to process large-value and/or high-priority payments made between participants in the system for their own account or on behalf of their customers. Although, as a rule, no minimum value is set for payments made in such systems, the average size of such payments is usually relatively large. During 2018, three systems settled 142 million payments with a total value of €489 trillion in euro payments, with TARGET2 and EURO1/STEP1 being the two main LVPSs5.

The full set of payment statistics can be downloaded from the Statistical Data Warehouse (SDW). The “Reports” section of the SDW also contains pre-formatted tables with payment statistics for the last five years. The data are presented in the same format as in the former “Blue Book Addendum”. For detailed methodological information, including a list of all data definitions, please refer to the “Statistics” section of the ECB’s website.

As a result of the progressive implementation of the Single Euro Payments Area (SEPA) and other developments in the payments market in Europe, the methodological and reporting framework for payments statistics has been enhanced as of the reference year 2014. The new requirements are laid down in the Regulation on payments statistics (ECB/2013/43) and in the Guideline on monetary and financial statistics (recast) (ECB/2014/15). A background note, available on the ECB’s website, describes the changes in more detail.

In addition to annual payments statistics for 2018, this press release incorporates minor revisions to data for previous periods. The hyperlinks in the press release are dynamic; thus, the data might slightly change with the next annual release due to revisions. Unless otherwise indicated, statistics referring to euro area cover the EU Member States that had adopted the euro at the time to which the data relate.